The gig economy promised freedom, but nobody warned you about the health insurance nightmare that comes with it.

If you’re driving for Uber, freelancing as a graphic designer, or running your own consulting business, you’ve probably discovered the harsh reality: traditional employer health benefits don’t exist in your world. And with open enrollment season approaching, the pressure to figure out affordable coverage is mounting.

Here’s the truth most gig workers learn the hard way – the traditional health insurance system wasn’t built for people like you. But smart independent contractors have discovered three game-changing strategies that can save both money and stress during enrollment season.

Why Traditional Health Insurance Fails Gig Workers

You’re caught in the perfect storm of health insurance challenges.

Unlike traditional employees who get subsidized group plans through their employers, gig workers face the individual market – where premiums can feel astronomical and options overwhelming. The typical advice of “just get an ACA plan” often falls short when you’re dealing with:

- Unpredictable income that makes budgeting for fixed premiums nearly impossible

- No employer contribution to help offset costs

- Complex marketplace navigation without HR support

- Limited understanding of what coverage you actually need as a healthy, active professional

Most gig workers end up either overpaying for coverage they don’t need or going without insurance entirely – both risky financial decisions.

What Happens When You Get It Wrong

The consequences of poor health insurance decisions compound quickly for independent workers.

Consider what happens when gig workers make common enrollment mistakes:

The Overpayer’s Trap: Many freelancers default to comprehensive ACA marketplace plans, paying premium prices for extensive coverage they rarely use. They’re essentially subsidizing benefits designed for families and older adults while struggling to maintain cash flow for their businesses.

The Coverage Gap Crisis: Others choose bare-minimum plans or go uninsured, only to discover that a single emergency room visit or unexpected health issue can wipe out months of earnings. Without employer-provided sick leave, any health setback becomes a double financial hit.

The Marketplace Maze: The annual scramble through Healthcare.gov leaves many gig workers confused and frustrated, often settling for the first plan that seems affordable without understanding the true costs or limitations.

The Subsidy Miscalculation: Fluctuating gig income makes it nearly impossible to predict annual earnings accurately, leading to subsidy repayment surprises at tax time.

These scenarios play out thousands of times each enrollment period, leaving hardworking independent professionals feeling trapped between inadequate coverage and unaffordable premiums.

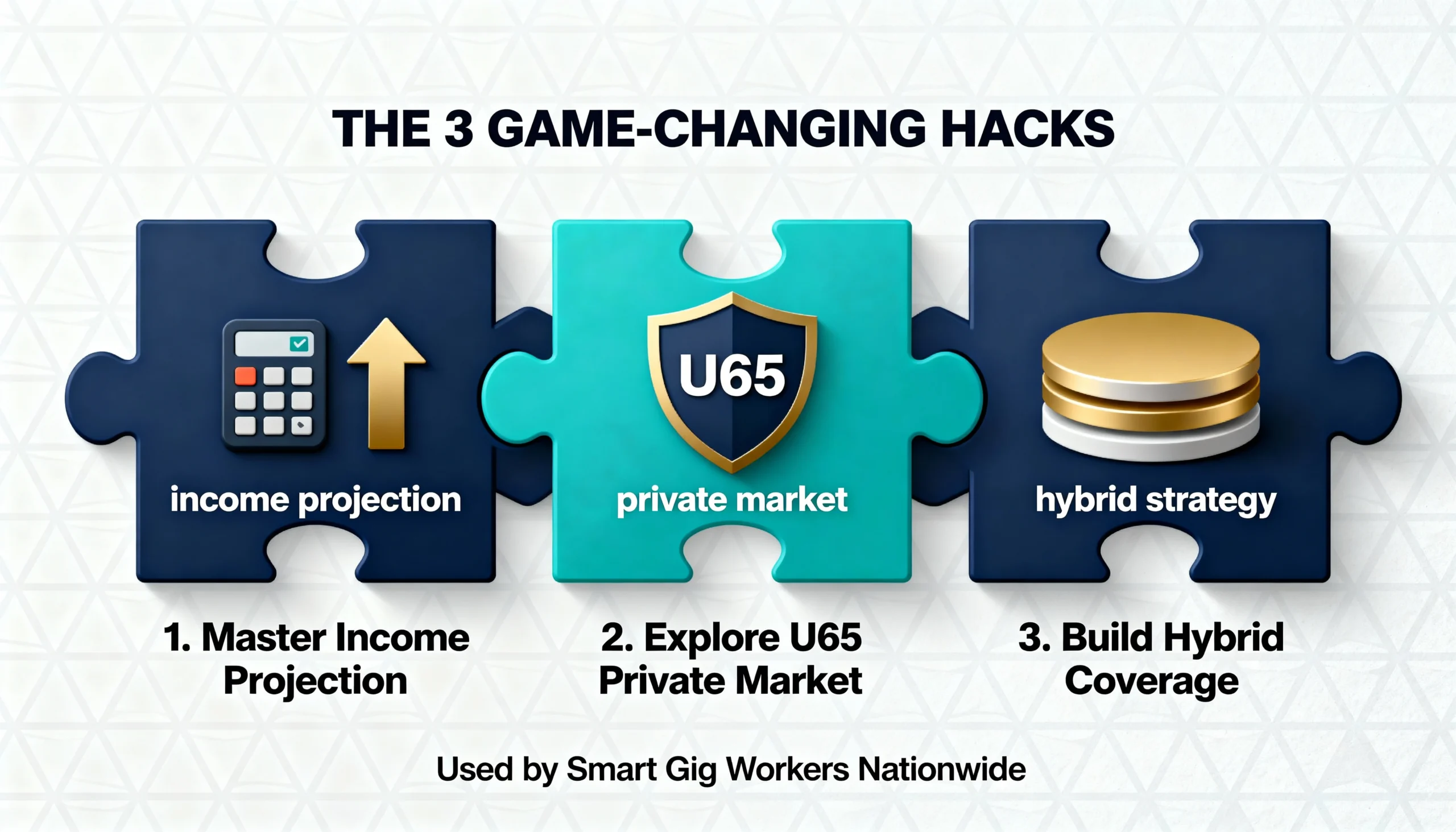

3 Insurance Hacks That Change Everything

Smart gig workers have cracked the code on affordable, flexible health coverage.

Hack #1: Master the Income Projection Game

The key to maximizing ACA subsidies lies in understanding how to project your variable income strategically. Instead of guessing at your annual earnings, successful gig workers:

- Track monthly patterns from previous years to identify seasonal trends

- Calculate conservative estimates that account for business fluctuations

- Understand the reconciliation process to avoid surprise tax bills

- Plan for income changes throughout the year

Hack #2: Explore the U65 Private Market Advantage

While everyone talks about ACA marketplace plans, savvy gig workers investigate private U65 health insurance options that often provide:

- More flexible enrollment periods beyond the traditional open enrollment window

- Customizable coverage levels that match your actual healthcare usage

- Potentially lower premiums for healthy individuals

- Streamlined application processes without marketplace complexity

Hack #3: Build a Hybrid Coverage Strategy

The most successful independent contractors don’t rely on a single insurance solution. Instead, they create layered protection through:

- Short-term coverage for gaps between longer-term plans

- Health sharing plans as primary coverage with traditional insurance as backup

- Supplemental policies for specific risks like accidents or critical illness

- Health Savings Accounts to maximize tax advantages and build medical reserves

![]()

Why These Strategies Work for Independent Professionals

These hacks address the unique challenges gig workers face in the health insurance market.

Unlike traditional employees with predictable schedules and steady paychecks, independent contractors need insurance solutions that match their lifestyle:

- Flexibility to change coverage as business needs evolve

- Cost control that aligns with variable income streams

- Simplicity in management without HR department support

- Value optimization that matches coverage to actual usage patterns

The most successful gig workers treat health insurance as another business expense to optimize, not just a necessary evil to endure.

Take Control of Your Health Insurance Future

Open enrollment doesn’t have to be a source of stress and confusion.

Understanding these strategies puts you ahead of most gig workers who struggle through enrollment season without a clear plan. The key is starting your research early and exploring all available options rather than defaulting to the most obvious choices.

Whether you’re a seasoned freelancer or new to the gig economy, having the right health insurance strategy can provide peace of mind and financial protection that lets you focus on growing your business.

Ready to explore your options? *Every gig worker’s situation is unique, and the best coverage strategy depends on your specific circumstances, health needs, and business goals. Feel free to reach out with questions about how these strategies might work for your situation – there’s no obligation, just helpful guidance from professionals who understand the independent contractor landscape.*